Anyone with even a vague interest in matters fiscal (or those with little real interest but some responsibility) is now awaiting next Tuesday’s pre-election fiscal update (PREFU).

PREFU is a good to have, and much better than nothing, but could be made quite a bit more useful and relevant for what must be presumed to be its ultimate purpose, informing the pre-election debate around matters fiscal. The current law governing PREFU is a single (full page) clause in the Public Finance Act.

For a start, it should probably be moved a week or two earlier. The law requires as follows

The Minister must, not earlier than 30 working days, nor later than 20 working days, before the day appointed as polling day in relation to any general election of members of the House of Representatives, arrange to be published a pre-election economic and fiscal update prepared by the Treasury.

which would be fine if we thought of polling day as 14 October. 12 September (next Tuesday) is more a month before that. But since that law was passed, advance voting has, for good or ill (I think mostly ill), come to make up a very large share of votes cast, and advance voting opens less than 3 weeks after the PREFU will be brought down. Changing the law to require the PREFU to be published 20-25 working days before polling opens would seem consistent with the spirit of the original legislation now that voting arrangements/patterns have changed so markedly.

Obviously there are trade-offs. There are significant lags involved in bringing the Treasury EFUs together, but the point of the exercise is to inform voters and enable scrutiny, debate, and challenge, including around political parties’ programmes in response to the PREFU numbers (this is mainly an issue for Opposition parties, as the governing party not only has the advance information from Treasury but can ensure some of its policy stance is included in the PREFU numbers themselves, when communicated to Treasury as government policy (eg stance of future operating allowances)). Note that the PREFU is not, and cannot realistically be counted on as, the “opening of the books” for an incoming government, because in unsettled times numbers can move about quite a bit even in the period between PREFU numbers being finalised and a new government taking office (this was an issue in 2008 for example).

PREFUs look a lot like the Budget and Half-Yearly economic and fiscal updates (BEFUs and HYEFUs) – here is the link to 2020’s and here is 2017’s (one prepared in more settled times) That is encouraged by law, since the things Treasury has to cover in each of these documents is the same. In respect of the economic forecasts, that is probably fine: after all, forecasts of the overall economy are just that: forecasts. A myriad of private choices, here and abroad, and the cyclical stabilisation activities of central banks, will influence outcomes, but mostly those outcomes are beyond the government’s (or Treasury’s) control. The economic outlook is a backdrop for fiscal numbers and, perhaps, fiscal policy.

I’m sure there will be some gotcha-type focus next week on some of the macro numbers. Will, or won’t, Q2 be shown as having experienced positive GDP growth. Given (a) the long lag on Treasury’s numbers, and b) that the actual official SNZ estimate is out the following week, much of that might be good fun but largely pointless. Same probably goes for their view on near-term inflation (if you could ask the Treasury forecasters next Tuesday their best guess of Q3 inflation it would almost certainly be different by then to what will be in the document they publish that day). That’s inevitable.

The real focus is, or should be, on the fiscal situation, which one or other party will be directly responsible for in a few weeks’ time (and one party is of course responsible now).

The operative bit is 26U(2) above. Hence, the government’s fiscal announcements last Monday, trimming future operating allowances etc, in ways quantifiable enough to be included by Treasury in the fiscal forecasts we will see next week. The Minister of Finance could, if s/he were sufficiently cynical, set the future operating allowances to zero and Treasury would have to include that “government policy” in its PREFU fiscal forecasts. The Secretary to the Treasury does not have any leeway to forecast how that policy might actually play out over several years. It is her legal responsibility simply to ensure that the forecasts accurately reflect the policy the Minister has communicated to her.

In the normal EFUs there is somewhat more restraint on Ministers of Finance. You could communicate to The Treasury low operating allowance numbers for this EFU but….you will still be minister in a year or two’s time and will be accountable for the eventual numbers. It isn’t perhaps much of a restraint – forward fiscal paths often have a “line on a graph” quality to them (with no specifics as to how these numbers will be delivered) – but it is something. In a pre-election EFU, no one is accountable for anything really (well, the Secretary is, but for faithfully representing government policy in the tables).

In the 2020 PREFU there was a bit of sensitivity analysis published – we were in the midst of pretty extreme Covid uncertainty at the time – but more normally there appears to be little or none (check again 2017’s and you will find none re the fiscal position itself, only (buried deep in supporting documents) on the cyclical adjustment estimates).

My focus here is not so much on the uncertainties of this year’s tax take. They are no doubt real, but economic cycles ebb and flow. Fiscal analysis really should focus mostly on cyclically-adjusted concepts and numbers.

But what we don’t get from Treasury in the PREFU documents – or anywhere else (other perhaps than in the periodic long-term fiscal report, which isn’t focused on the next 2-4 years) – is any sense of the state or implications of the cost pressures that will be difficult for any party in government to avoid. Political parties can and should debate what programmes should be provided and what not. Treasury can’t offer any particular insight on those debates. But it can, and should, be offering some sense of the spending implications of projected population growth, projected inflation, projected private sector real wage growth, and so on. If the past is any guide, next week’s PREFU will show us none of that. The revenue implications will be taken into account but, except where the law requires indexation (for example), not the expenditure implications. Unless conscious and deliberate other choices are made, those sources of pressure will increase government spending over time. But Ministers of Finance are simply free to give the Secretary to the Treasury a path for future operating allowances which need not bear any relationship to, or be based on any analysis of, largely inescapable cost pressures.

This might be seen primarily as a dig at the current government. It isn’t. In 2017 there was a huge political and analyst debate about alleged Labour “fiscal hole”. Many of the claims proved to be overblown but the “largely inescapable cost pressures” point was very real. At the time, and at the prompting of several former senior Treasury officials, I wrote a post on exactly that issue. By that time we had both the PREFU (reflecting incumbent government’s plans and operating allowances) and the then Opposition’s own fiscal plans (at present we have numbers from neither side). This text and chart was from that post

and after I’d worked through various detailed numbers around forecast influences that would boost costs

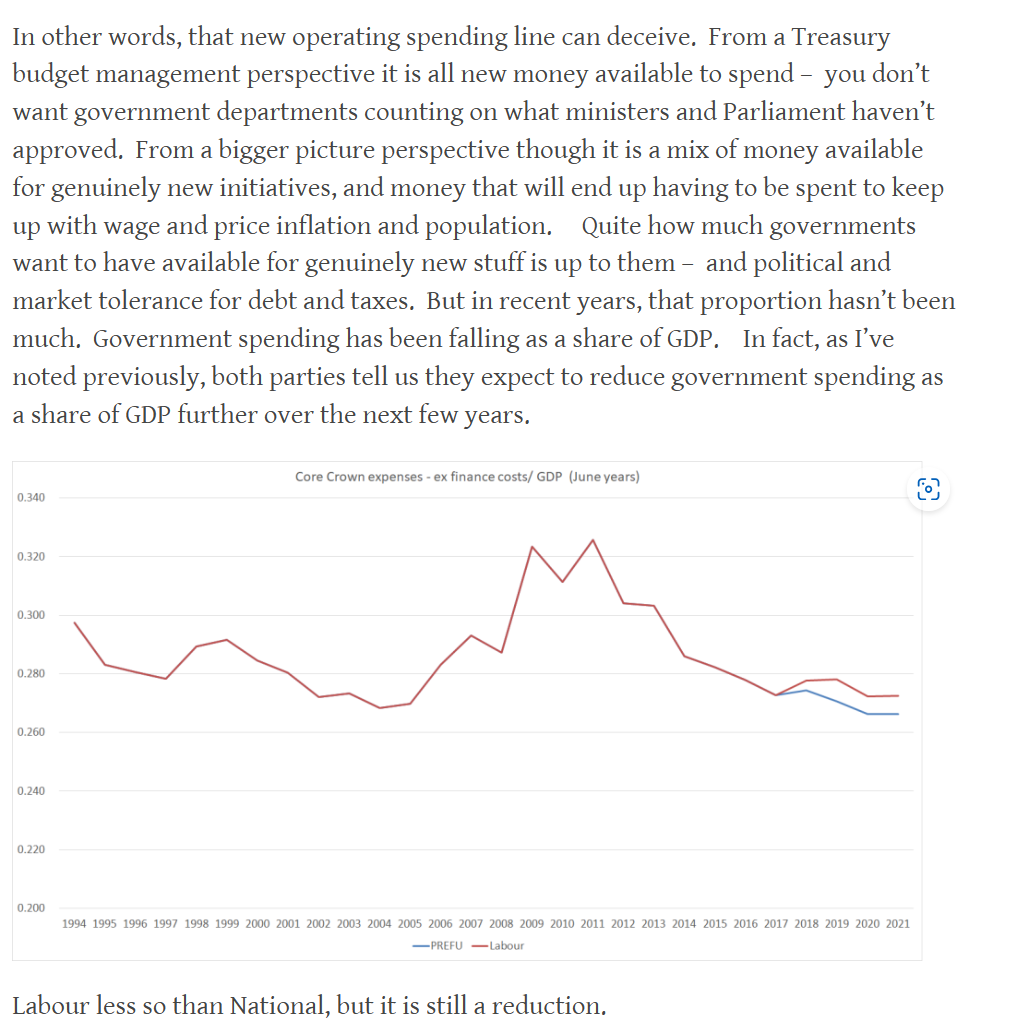

Neither side told us how they envisaged reducing government spending as a share of GDP. In a mechanical sense (PREFU and Labour’s parallel) they added up, but in substance they didn’t. Some related points were also in this post.

I expect that in next week’s PREFU there will be an operating surplus shown at some point in the relevant horizon (perhaps a year later than was suggested in the Budget). Quite probably – given that National seems to have no interest in an aggressive fiscal consolidation – that will suit both parties, but in both cases it will avoid the hard discussions around the choices that will bring about such surpluses. Countries don’t get from cyclically-adjusted deficits to surpluses by magic – or by simply drawing a line on a graph. Both sides are already guilty of “line on graphism” with what are no more than assumptions about savings that might be made without addressing programmes or choices that would make such savings sustainable.

It isn’t that medium-term fiscal projections are always useless. Sometimes legislation will already have been passed that will come into effect only gradually, and we want to be able to see the implications of those legislated commitments. But that really isn’t much of an issue at present. And absent such slowly unfolding adjustments it really means that almost no attention should be paid to any fiscal deficit numbers in PREFU beyond the current financial year: this year’s Budget has been passed and what is authorised isn’t vapourware. But what parties tell us vaguely they might do in future (and both are guilty) isn’t really worth much at all.

I ended that 2017 post with this suggestion

I stand by that call. I’m quite confident there has been a lot of very low quality spending in recent years, but I also suspect that the things governments need to spend money on are benefiting temporarily from the big surprise inflation. I’ve made the point here that teachers were more or less forced to accept a real wage cut, and a big cut relative to private sector wage developments. Recruitment and retention challenges are, shall we say, not unknown in the sector, and if we care at all about a high quality education sector then over time (and whatever else needs sorting out) we will need to pay accordingly. The senior doctors dispute seems to have similar characteristics. But how large and pervasive are these effects across the board? Treasury is best-placed to know, and to tell us. If the amounts are material then whatever savings can be made from genuine bloat might not reduce deficits at all but just end up having to be spent to be able to maintain or secure high quality core services. Treasury is obliged to publish a lot, but it could publish more and more useful standardised information along these lines.

[…] Making the PREFU more useful […]

LikeLike